Have you ever transferred money to an adult child and immediately felt two things at once?

Relief that you could help. And a quiet dread about what it just cost your future.

If that is familiar, you are not alone. And you are not weak. You are caught in the middle of one of the most financially and emotionally complex situations a Canadian parent can face right now.

I have been in this industry for over 24 years. I have five children. I raised them as a single dad through some of the hardest financial years of my life. And I will tell you honestly: I never thought I would still be writing cheques, sending e-transfers, and figuring out how to help them in their adult years.

But here I am. And I am not pretending otherwise.

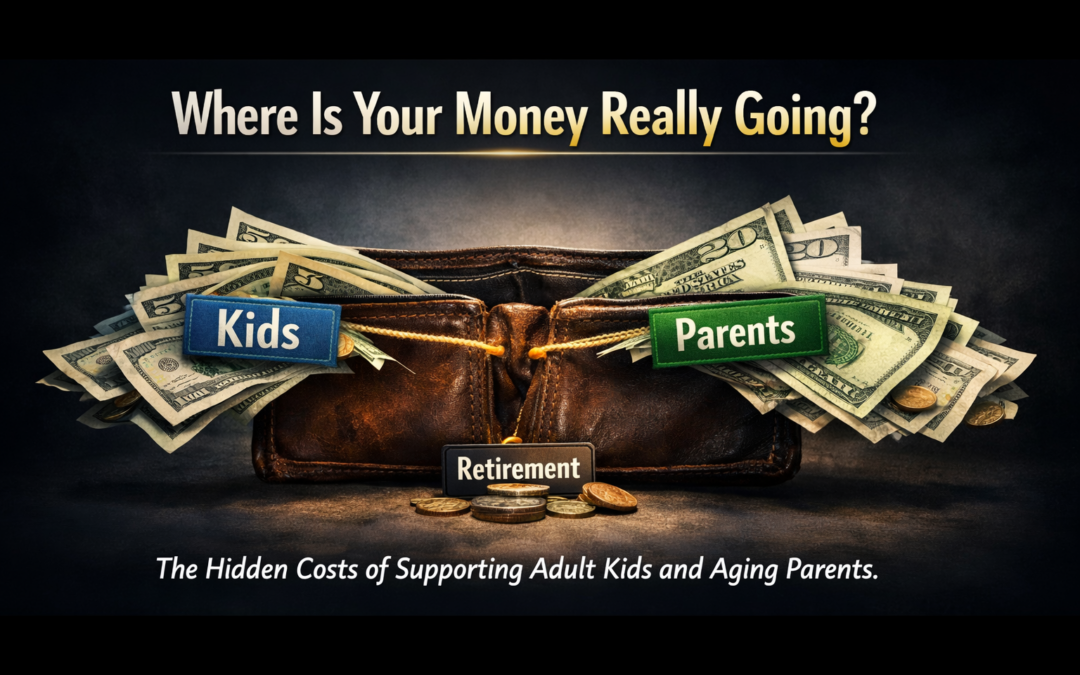

This is the conversation I have been turning over for a long time, because I am living a piece of it myself. The topic is what gets called the sandwich generation. Parents who are financially and emotionally caught between supporting their adult kids on one side and supporting, or preparing to support, their ageing parents on the other.

The title sounds tidy. The lived experience is anything but.

The Numbers Behind the Pressure

In November of 2025, a polling firm called Ipsos released a study conducted for RBC that put a number on something I have felt in my chest for years.

53% of Canadian parents of kids aged 13 to 24 feel negatively about their children’s financial future.

71% say that stress about their kids’ finances is affecting their own well-being.

Think about what that actually looks like from the inside. It is not just a statistic. It starts as quiet desperation on a Tuesday afternoon when you are doing mental math at your desk. It shows up in a short fuse with your spouse over something small. It shows up at 3:00 AM when you are staring at the ceiling and cannot tell your brain to stop.

And the part that does not show up in that survey, but shows up in my practice every single week, is this: the parents who are losing sleep are the same parents who are quietly raiding their own retirement to keep their adult kids afloat.

That is the problem I want to talk about today.

Why Your Kids Are Not Failing

Before we go any further, I want to say something clearly because I think it matters.

My kids are not lazy. They are working; they are trying. But the world they are trying in is not the world I started in.

Statistics Canada tells us that more than one in three Canadian young adults under the age of 34 are living with at least one parent. In Ontario, it is over 40%. In Toronto, nearly half. Across British Columbia and Alberta, the rates climb every year.

Because the alternative for many of them is spending 60, 70, sometimes 80% of their take-home pay on rent alone. Before food. Before transportation. Before a single dollar reaches their own future.

That is not a moral failure on the part of young adults. That is math.

So they stay home, or they come back home, and the parents make space. And that is fine. That is healthy in many cultures and has been for generations.

But here is what the data also tells us. Statistics Canada released a study this year showing that in these intergenerational households, the financial support flows primarily from the older generation down. The parents are subsidising. And parents between the age of 65 and 69 living with their adult children have a 32% employment rate, compared to 24.6% for others in that age group.

Parents who should be retired, who have earned their retirement, are working into their late sixties because their adult kids still need help.

That is the sandwich. And it is getting thicker.

The Three Withdrawals Nobody Puts on a Statement

I want to walk you through what I call the three withdrawals. These are the three ways the sandwich generation quietly bleeds their own financial future without realising it, because nobody is putting a number on it as it happens.

-

Direct Financial Support

Cell phone bills, car insurance, groceries when they visit, the occasional emergency loan that never quite gets repaid. None of it feels like a big deal in the moment. A hundred dollars here, two-fifty there. But added up over a year, many parents are spending $5,000 to $10,000 annually supporting adult kids. Multiply that by 10 years and you are looking at $50,000 to $100,000 that did not go into your TFSA, your RRSP, or any vehicle that compounds for your retirement.

-

Opportunity Cost

This one is more invisible than the first. When parents redirect money toward their kids, they often skip their own contributions. Year after year. They tell themselves they will catch up later. But there is no catching up when it comes to compounding. A dollar you do not invest in your forties is not a dollar you lose. The compounding you forfeit when you pause your own savings to fund somebody else’s life is the most expensive money you will ever not spend on yourself.

-

Delayed Retirement

This is the one that breaks my heart most when I am working through my clients’ challenges. Parents in their early sixties tell me they will just work a few more years. That is a fine plan until your body decides otherwise. Until your employer decides otherwise. Until your spouse’s health changes everything overnight. The reality is that most Canadians do not retire on their chosen date. They retire on a date that gets chosen for them. And if you have leaned on the assumption of working until 68 or 70 and something forces you out at 62, the gap between what you have and what you need can be devastating.

These three withdrawals do not show up on a statement. There is no line item that says you sacrificed $60,000 of compounded retirement growth to subsidise your son or daughter’s rent. But the dollars are gone all the same.

The Question Most Parents Have Never Asked Out Loud

Here is where I want to push past the numbers, because if I give you numbers and stop, I have only done half the job.

The other half is the harder question: what do you actually want your life to look like on the other side of this?

Most of the clients I sit down with have never asked themselves that question out loud. They are running on autopilot. Adult kid needs help. Send the e-transfer. Parent needs something. Figure it out. Spouse mentions retirement. Change the subject.

That is living by accident.

Living on purpose means stopping long enough to ask three questions.

-

What kind of parent do I want to be to my adult children?

Not what they want me to be. Not what guilt tells me I should be. What I actually want to be. Because there is a version of helping that grows people up, and there is a version that keeps them small. I would argue gently that handing over money without conversation tends to keep them small.

-

What kind of son or daughter do I want to be to my ageing parents?

If that is becoming part of my picture, have I had the hard conversations? Do I know if they have a will? Do I know if they have power of attorney in place? Do I know what their wishes are if their health changes? Because the time to ask is not the day after the stroke.

-

What do I want my own retirement to look like?

And am I willing to actually protect that vision instead of giving it away one transfer at a time?

Living on purpose means having the courage to say to your adult child, I love you. And the answer is no. Or yes, but with conditions. Or yes for three months, and then we sit down again. That is not unkind. That is parenting an adult.

Have the Conversation Before the Crisis Does

Here is what I want you to do this week. Not a worksheet. Not a download. A conversation.

If you have adult kids you are supporting, sit them down. Not in anger, not in frustration. With love. And say something like this:

“I love you. I want to keep helping you. And I need to be honest with you about what that help is costing me. I am not retiring on schedule if this continues. I need us to look at this together, set a timeline, and build a plan that gets you to independence and protects my future at the same time.”

That conversation, done well, will change your family. The adult child does not feel attacked. They feel respected. And often they did not realise the weight they were placing on you, because you never put it into words.

And if you have ageing parents, have a different conversation. Ask about the will. Ask about the powers of attorney. Ask what they would want if their health changed. Not because you are morbid. Because you love them. And because the cost of waiting until a crisis to ask these questions is measured in dollars and in heartbreak.

The Sandwich Generation Pressure Is Real. So Is the Way Through.

When I look back at my own financial journey, the years I was a single full-time dad living paycheque to paycheque, the years I figured out how money actually works, and the years now where I am supporting some of my adult kids while also trying to build something I am proud to leave behind, I keep coming back to one truth.

Living on purpose is not a one-time decision. It is a daily choice.

It is a choice to know your numbers. It is a choice to have the conversation you have been avoiding. It is a choice to say yes when yes is right, and no when no is right, and to do both with love.

The financial weight is real. The emotional weight is real. But you do not have to carry it by accident. You can carry it on purpose.

And those are two completely different lives.

Are you caught in the middle right now? Or can you see it coming? Drop a comment below. I read every one, and this is a conversation worth having out in the open.

Connect with Dwight Heck

giveaheck.com | Give A Heck Podcast — available on Spotify, Apple Podcasts, YouTube, and everywhere you listen

Licensed to help clients in Alberta and British Columbia. Available to consult with families anywhere on the financial questions that follow you, regardless of where you live.